Property Edge

What’s Next for Property Prices in 2025?

Welcome to this week’s edition of The Property Edge, where we explore the latest trends shaping Australia’s property market and economy. From rising property prices forecast for 2025 to affordable investment opportunities for everyday Australians, we’re covering it all. We’ll also dive into the OECD’s bold predictions for interest rate cuts and examine how public spending is keeping Australia out of recession—but at what cost? Whether you’re an investor, homeowner, or just curious about the state of the market, this issue has the insights you need to stay informed.

QUICK HEADS-UP: Before we get into the details, we wanted to share something important.

Find Off-Market Motivated Sellers and Automatically Calculate Potential Profits with Fast Property AI – Free Access Now!

Our research tool helps you find off-market motivated sellers and calculates potential flipping profits. We have a handful of have trial licences available to trial, available now! No credit card required.

Click here to get immediate access

Back to the newsletter…

What’s Next for Property Prices in 2025?

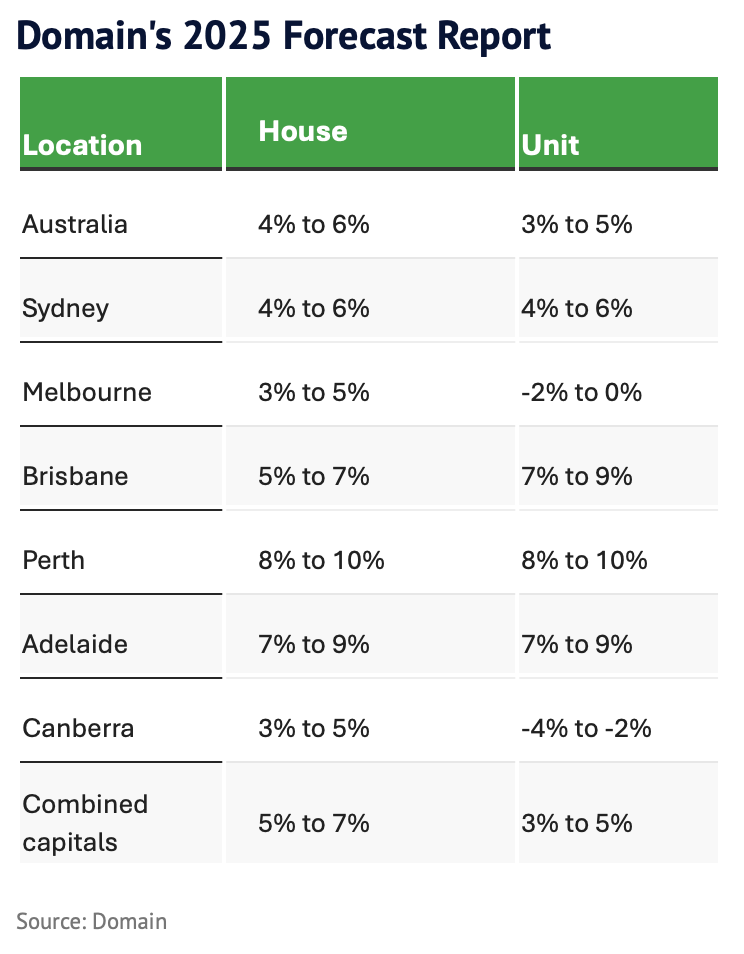

Australian property prices are predicted to rise by up to 6% in 2025 if interest rates are cut, according to new forecasts. A chronic housing shortage combined with ongoing demand is expected to sustain growth, albeit at a slower pace, as affordability pressures mount.

The Domain 2025 Forecast Report projects a national average increase in house prices between 4% and 6%. Sydney’s house and unit prices are forecast to follow this trend, while Melbourne is expected to see weaker growth of 3% to 5% for houses and no growth or slight declines of up to 2% for units.

Top Performers

Perth is poised to lead the nation with house and unit prices projected to rise by 8% to 10%, followed by Adelaide with anticipated growth of 7% to 9%. Brisbane is also expected to perform strongly, with house prices increasing by 5% to 7% and unit prices climbing by 7% to 9%.

A Year of Two Halves

Domain’s Chief of Research and Economics, Dr. Nicola Powell, anticipates a split market in 2025.

“Growth is expected to ease in the first half of the year, as buyers continue to hold back,” Powell said. “However, the second half could see stronger momentum as rate cuts are introduced, economic sentiment improves, and buyer confidence returns.”

She emphasised that persistent supply shortages, construction challenges, and strong demand for home ownership will underpin price growth across most regions.

Focus on Affordable Markets

Smaller capital cities such as Perth, Brisbane, and Adelaide are expected to outpace the national average, driven by affordability and population growth. Entry-level markets in Sydney and Melbourne could also see increased activity, spurred by the federal government’s newly approved Help to Buy scheme.

Broad Market Alignment

The forecast aligns with projections from major banks, including NAB (4.2% growth), CBA (5%), Westpac (3%), and ANZ (5%-6%). ANZ senior economist Adelaide Timbrell highlighted the role of mid-sized cities in driving growth, noting that population booms have outpaced housing supply in these regions.

Sydney and Melbourne are expected to see slower growth due to their already high price levels. However, interest rate cuts, wage growth exceeding inflation, and recent income tax cuts are expected to boost borrowing capacity and support property prices nationwide.

What to Watch

While the overall outlook is positive, regional variations will continue. The ongoing affordability crisis, construction challenges, and economic conditions will shape the trajectory of property markets across Australia in 2025.

Invest Here: 44 Suburbs Within Reach for Average Australian Investors

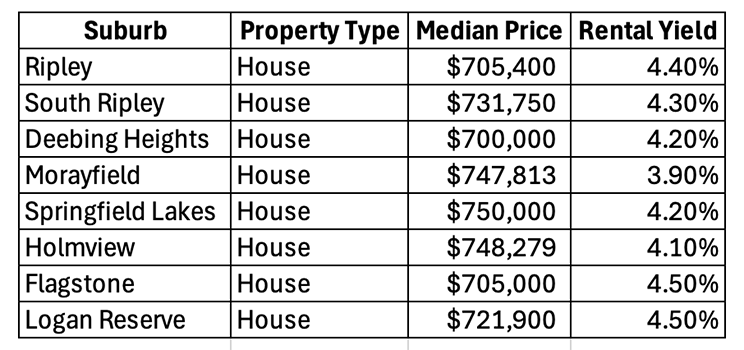

From Ripley on the outskirts of Brisbane to coastal Perth and booming satellite suburbs of Sydney, 44 affordable locations across Australia have been identified where investors on an average income can still afford to enter the property market.

Investment advisor John Fitzgerald of JLF Group explains that contrary to popular belief, you don’t need to be “rich” to invest in property.

“There is a misconception that every property investor in Australia is wealthy or a high-income earner; it’s just not true,” Fitzgerald said.

Data from the Australian Bureau of Statistics shows the average Australian couple working in the private sector earns $191,000 annually, while public sector workers earn a combined pre-tax income of $219,000. Using these figures and factoring in lending criteria, JLF Group has pinpointed affordable suburbs across Australia with strong potential for long-term growth.

Southeast Queensland

In southeast Queensland, suburbs such as Ripley, South Ripley, and Deebing Heights stand out for their affordability and growth potential. These areas, located within the Ipswich corridor, are supported by government infrastructure investment and population growth.

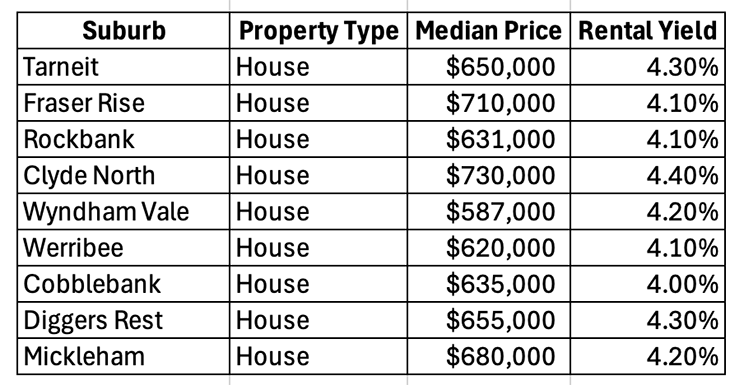

Victoria

Tarneit leads the way in Victoria, offering affordability, excellent infrastructure, and population growth. Nearby suburbs like Fraser Rise and Rockbank also stand out for their investment potential.

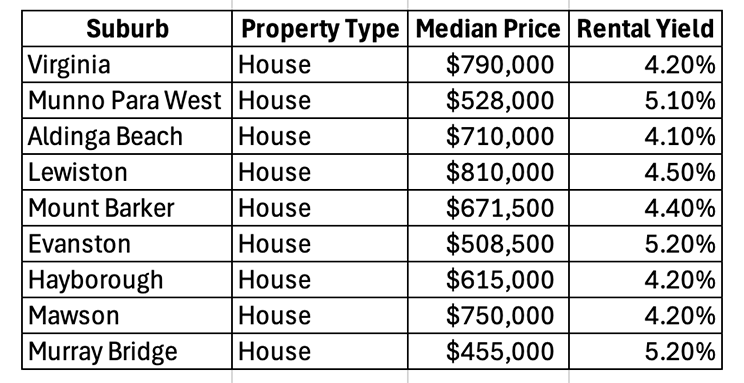

South Australia

In South Australia, suburbs in Playford such as Virginia and Munno Para are affordable with solid rental yields, and the region is well-connected to Adelaide’s transport network.

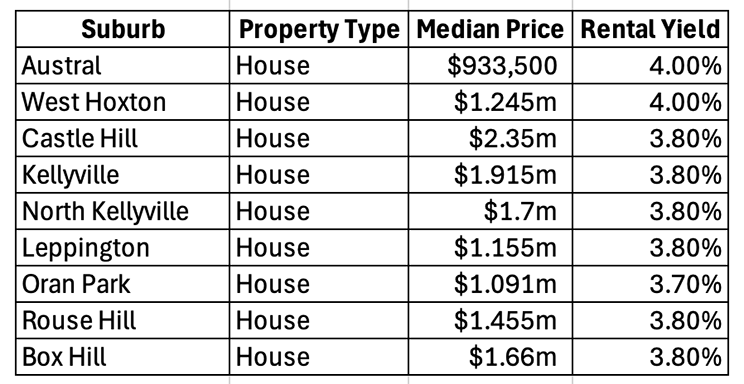

New South Wales

In NSW, outer suburbs such as Austral and West Hoxton offer growth potential, while established areas in The Hills District provide opportunities for long-term capital gains.

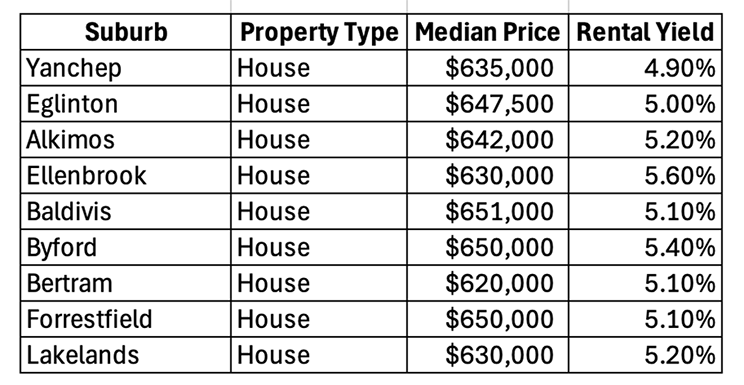

Western Australia

Western Australia offers excellent affordability and high rental yields, particularly in Yanchep and surrounding areas with strong population growth projections.

These affordable suburbs across Australia demonstrate that with the right strategy, property investment is achievable on an average wage, offering opportunities for steady growth and solid rental yields.

OECD Predicts Significant Interest Rate Cuts Over the Next Year

Australia may soon see a major shift in monetary policy, with the Organisation for Economic Co-operation and Development (OECD) predicting a full percentage point drop in interest rates over the next year.

In its latest outlook report, the Paris-based financial body, led by former Australian finance minister Mathias Cormann, forecasts the Reserve Bank of Australia’s (RBA) cash rate will decrease to 3.35% by early 2026.

“An easing of monetary policy is warranted over the next year given ongoing disinflation and below-potential growth,” the OECD wrote.

The report cites falling inflation and stagnant nominal policy rates since November 2023 as key reasons for the expected cuts. It predicts headline and core inflation will return to target levels by early 2025, allowing the RBA to begin gradual rate reductions next year.

What This Means for Borrowers

The OECD’s forecast aligns with predictions from Australia’s major banks, most of which expect up to four rate cuts in 2025. However, ANZ has recently tempered its outlook, forecasting just two cuts.

Lower interest rates could bring relief to borrowers after a prolonged period of high costs, though the OECD cautions that inflation remains a potential hurdle. If inflation stays higher than expected, the RBA may be forced to maintain or even increase rates.

Economic Growth and Immigration Policy

The OECD also projects Australia’s economic growth will improve modestly, rising to 1.9% in 2025 and 2.5% in 2026, up from just 0.8% in the 12 months to September 2024.

However, it warns that proposed immigration restrictions aimed at addressing housing pressures could backfire. Both the federal government and opposition have suggested cutting migration numbers, but the OECD highlights that such measures could stifle consumption growth and worsen labour shortages, particularly in the construction sector.

“Policymakers should beware, in seeking to curb immigration to ease pressures on housing costs, of worsening labour shortages, including in house-building,” the OECD cautioned.

What’s Next?

If inflation remains under control, Australians could benefit from lower interest rates and a stronger economy in the coming years. However, the balance between housing affordability, immigration policy, and economic growth will remain a critical challenge for policymakers to navigate.

Australia’s Economy Relies on Public Spending to Avoid Recession

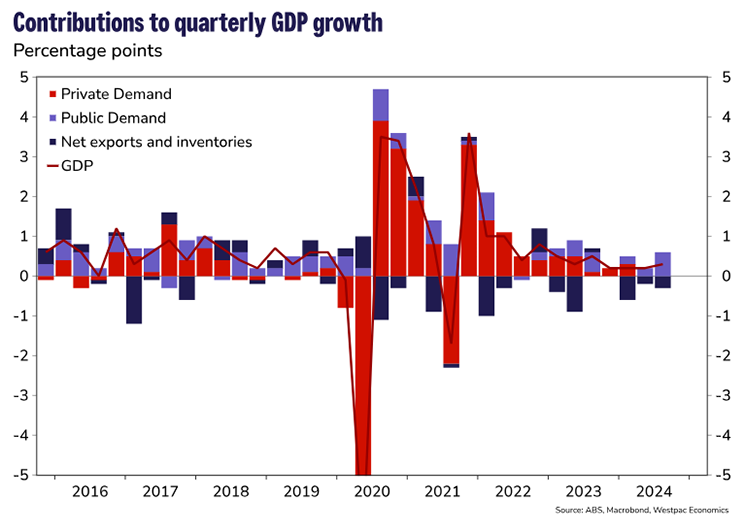

A stark reality has emerged in Australia’s latest economic growth figures: without rising public spending, the nation would already be in a technical recession. As highlighted in the accompanying graph from Westpac’s economics team, government demand has been the sole driver of GDP growth over the past two quarters, offsetting a shrinking private sector.

The purple columns, representing public sector demand, have effectively kept the economy afloat. Remove them, and Australia would have experienced two consecutive quarters of contraction—commonly defined as a recession.

Government Spending Fills the Private Sector Gap

Reserve Bank Governor Michele Bullock has acknowledged the critical role of government spending. Speaking recently, she explained:

“The private sector in Australia at the moment is very weak, and the public sector demand has been filling that gap.”

Bullock defended the increase in public sector employment—such as teachers, nurses, and aged care workers—arguing these roles are essential to both the economy and society.

“If [public spending] wasn’t filling that gap, then things might well be much worse in terms of the employment market,” she said.

Interest Rate Cuts: A Double-Edged Sword

While public spending is propping up the economy, it’s also delaying interest rate cuts. The Reserve Bank has maintained the cash rate at 4.35%, citing a strong jobs market (with unemployment at just 4.1%) and persistent demand as reasons inflation isn’t falling faster.

The OECD and major banks predict rate cuts will begin in 2025, but had government spending been lower, cuts may already have occurred. However, the trade-off would likely have been higher unemployment and a deeper economic contraction.

CBA’s head of Australian economics, Gareth Aird, noted:

“Restrictive monetary policy has clearly worked to slow private demand growth in the economy.”

Despite slowing private consumption, record public spending—now at 27.5% of total economic output—continues to stabilise jobs and economic activity.

Australia vs. New Zealand: A Tale of Two Economies

Australia’s slow and steady approach contrasts sharply with New Zealand’s aggressive rate hikes, which pushed its economy into two technical recessions in just over a year. While the Reserve Bank of New Zealand took rates to 5.5%, Australia’s RBA capped its rate at 4.35%, prioritising employment stability.

New Zealand’s unemployment rate has risen from a pandemic low of 3.2% to 4.8%, and many Kiwis are migrating to Australia in search of better opportunities—a testament to the RBA’s cautious strategy.

As Australia navigates the complexities of economic recovery, the interplay between public spending and private sector growth remains a pivotal issue. While government intervention has helped stave off recession, the road ahead will require careful planning to balance stability and sustainable growth. Stay tuned to The Property Edge for ongoing analysis, expert insights, and the latest updates to help you stay ahead in a shifting market. See you next week!