Property Edge

Suburbs Where Investors Are Selling For A Loss

Hi Property,

Welcome to this week’s edition of Property Edge, where we bring you the latest insights, forecasts, and expert analysis shaping Australia’s property market. With interest rates still a hot topic and economic challenges impacting homeowners across the nation, this week’s update delves deep into predictions from economists, the Reserve Bank of Australia (RBA), and the Big Four banks. From interest rate forecasts to the latest government initiatives, we’ve got all the key developments you need to know.

Suburbs Where Investors Are Selling For A Loss

Homeowners, especially investors, are selling properties at a loss, particularly in high-density markets like Melbourne, Perth, Darwin, and Parramatta, where 30-40% of sales were below the original purchase price. This has been driven by an interest rate environment where cuts are not anticipated soon. Average losses range from 42,000 to 69,000, mostly in areas flooded with high-rise units.

Experts warn that potential reforms to negative gearing and capital gains tax could worsen the situation, leading to more investor sell-offs and a critical reduction in rental stock during a housing shortage caused by high migration.

Losses were heavily concentrated in areas with an oversupply of investor-owned properties, particularly in locations where buyers overpaid during market peaks. In Melbourne’s CBD, nearly 40% of sales resulted in losses, with a median loss of 64,000. In Perth and Darwin, over a third of sellers also sold at a loss. By comparison, Brisbane and Adelaide remain strong markets, with losses being relatively rare.

The situation is being compounded by investor distress, driven by the Reserve Bank’s hesitation to cut interest rates, making property ownership more expensive for those relying on rental income to cover costs. Many properties in these loss-making areas were originally purchased off-the-plan, often at inflated prices during a property boom, only for their values to fall in subsequent years.

Economists and industry professionals argue that changes to negative gearing could drive more investors to sell, worsening the rental crisis as the supply of rental properties diminishes. However, Prime Minister Anthony Albanese has clarified that the government is not planning to take negative gearing reforms to the next Federal election.

Experts, including SQM Research’s Louis Christopher, warn that reforming negative gearing would discourage investment and result in increased rental costs as landlords exit the market to cut losses, further suffocating the rental supply. This issue is part of broader concerns about the property market, with slow price growth reported in the latest PropTrack Home Price Index and certain regions like Hobart, Canberra, and Melbourne showing price declines compared to last year.

In summary, the challenges facing investors in these “danger” suburbs are part of broader economic and policy pressures that could exacerbate existing shortages in the rental market while driving more loss-making sales in high-density areas.

Contrasting Property Markets: Why Some Australian Cities Are Booming While Others Struggle

In September 2024, Australia’s home prices saw slight overall growth, but the gains were uneven. Cities like Adelaide, Perth, and Brisbane saw strong annual increases of 13% to 22%, driven by low supply and strong demand. In contrast, Melbourne and Hobart experienced declines, with Melbourne’s dwelling prices down 1.79% for the year. Supply shortages benefited sellers in Perth and Adelaide, while Melbourne’s abundance of listings pressured prices downward. Interest rate uncertainty and varying market conditions contributed to these differences in performance across the country.

The Return of Government Backed Help to Buy: How Australia’s Shared Equity Schemes Compare

The much debated Help to Buy bill is set to return to parliament this month, which would allow the federal government to co-purchase homes with about 40,000 first-home buyers. Most Australian states already have their own shared equity schemes. These programs, including Victoria’s Homebuyer Fund and WA’s Keystart, offer varying levels of government support. For instance, the federal scheme offers up to 40% for new homes and 30% for existing ones. Experts say these programs help ease the housing crisis but argue for broader reforms like changes to tax policy and negative gearing.

State Comparisons:

- New South Wales: Previously ran a pilot program targeting key workers and single parents, but it ended in June 2024.

- Victoria: The Homebuyer Fund offers up to 25% of a home’s price with a 5% minimum deposit, and First Nations participants can receive up to 35%.

- Queensland: Has passed legislation to support the federal Help to Buy scheme, but has no current shared equity program.

- South Australia: HomeStart provides up to 25% of the home price as an interest-free loan.

- Western Australia: Keystart has been running since 2007, offering up to 30% of the property price with a 2% deposit.

- ACT: A limited scheme for public housing tenants who must pay 70% of the home’s price.

- Tasmania: MyHome allows participants to borrow up to 40% of the property price for new homes and 30% for existing ones.

- Northern Territory: No shared equity scheme, but offers HomeGrown Territory Grants for first-home buyers.

Experts agree that while these schemes can make a difference, they are not the sole solution to Australia’s housing crisis. Broader reforms, including changes to tax policy and capital gains tax, are needed to address the issue at its core.

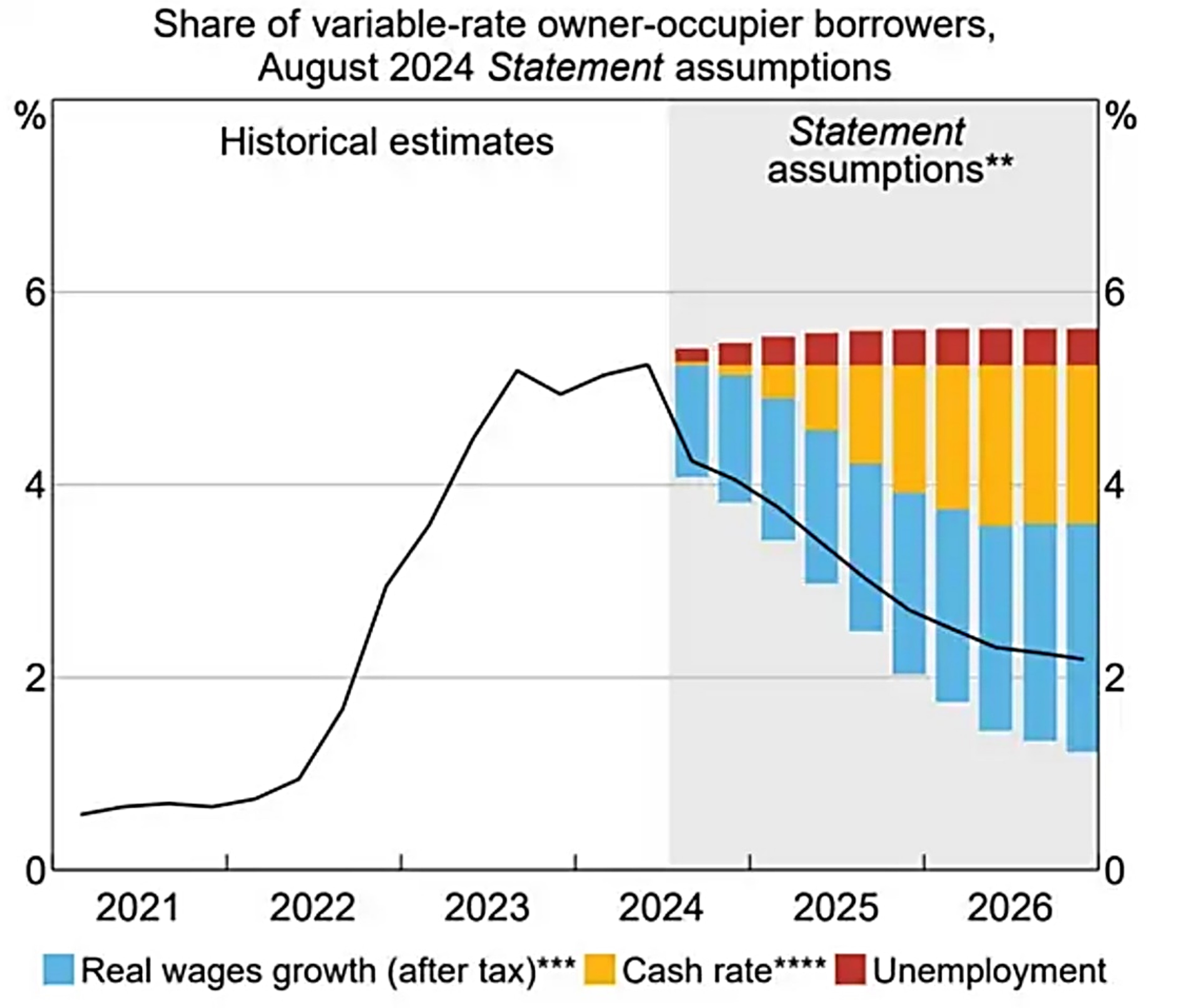

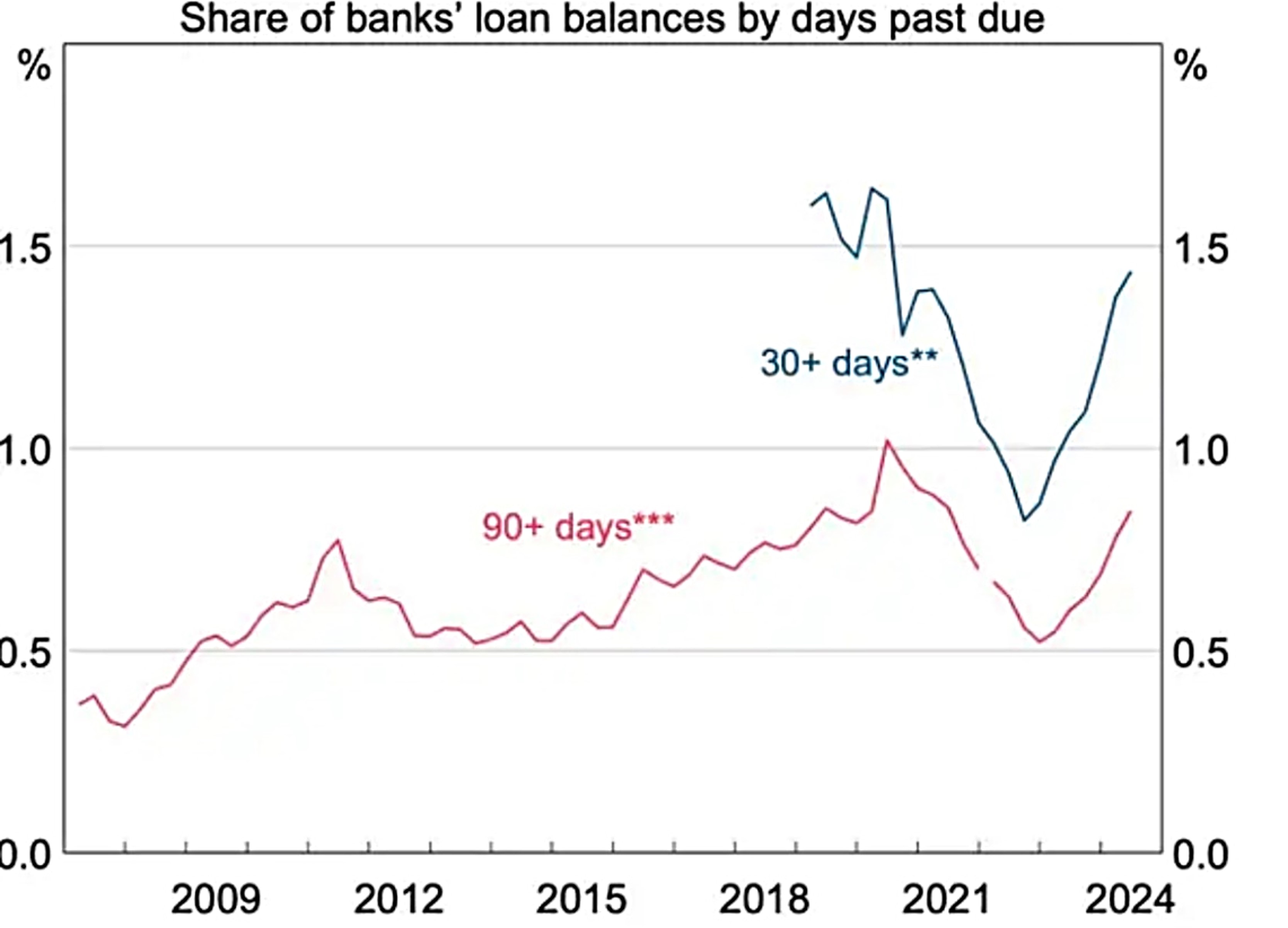

RBA Warns of Risks That Could Increase Mortgage Struggles for Australians

The Reserve Bank of Australia (RBA) has cautioned that the number of Australians facing mortgage stress could rise if the economy slows more than anticipated or if interest rates remain high. While most borrowers are managing their debts, around 5% of owner-occupiers with variable-rate mortgages are struggling to meet essential expenses and repayments.

Overseas risks, such as China’s economic slowdown, could also impact Australia’s financial stability. Despite these challenges, inflation is falling, and household budget pressures may ease later in 2024.

The Big Four banks are expecting rate cuts soon:

- Commonwealth Bank predicts the first cut in December 2024, with five cuts in total by the end of 2025, bringing the cash rate to 3.10%.

- Westpac anticipates a cut in February 2025, with four cuts in total, lowering the rate to 3.35%.

- NAB forecasts cuts beginning in May 2025 (possibly February), with a total of five cuts down to 3.10%.

- ANZ expects cuts starting in February 2025, with three cuts, bringing the rate to 3.60%.

As we continue to navigate an ever-changing property market, staying informed is key to making the best decisions. We hope this edition of Property Edge gives you the insights you need to stay ahead.

Warm regards,

Property Lovers Team

Find Your Next Property Deal in 30 Days or Your Money Back!

What if you could find your next profitable property deal in the next 30 days or less, risk-free?

Access to all the tools, training, and AI technology to secure a profitable property deal for potentially little to no money down, for less than a cup of coffee a day.

This is the moment you’ve been waiting for.

Click here to watch the full video and see Fast Property AI in action now.

Your AI team is waiting. All that’s left is for you to take action and join us.