Property Edge

RBA Maintains Cash Rate Amid Inflation Concerns

Welcome to this week’s edition of the Property Edge newsletter, where we keep you informed on the latest trends, insights, and opportunities in the Australian property market. As interest rates remain a hot topic and the number of million-dollar suburbs continues to rise, we’re here to break down what this means for property investors and how you can leverage these shifts to your advantage. From mortgage stress trends to the growing gap between house and unit prices, we’ve got the key insights you need to stay ahead in the ever-changing property landscape.

RBA Maintains Cash Rate Amid Inflation Concerns

The Reserve Bank of Australia (RBA) has kept the cash rate steady at 4.35% following its recent board meeting, marking the seventh consecutive hold. Despite inflation falling substantially, the RBA states it’s still above the 2-3% target range, suggesting potential for future rate hikes.

Implications For The Property Market

This hold means homeowners will continue to face the current 13-year high cash rate at least until the next review on 5th November. Canstar estimates that Australians are collectively paying an extra 5.52 billion in monthly mortgage repayments compared to March 2022.

Governor Michele Bullock reiterated that while the RBA won’t lower rates until inflation falls into their target range, she acknowledged the financial struggles faced by households. Particularly, the burden continues to fall on low-income and younger households, who may be pushed into selling their homes due to rising living costs and interest rates.

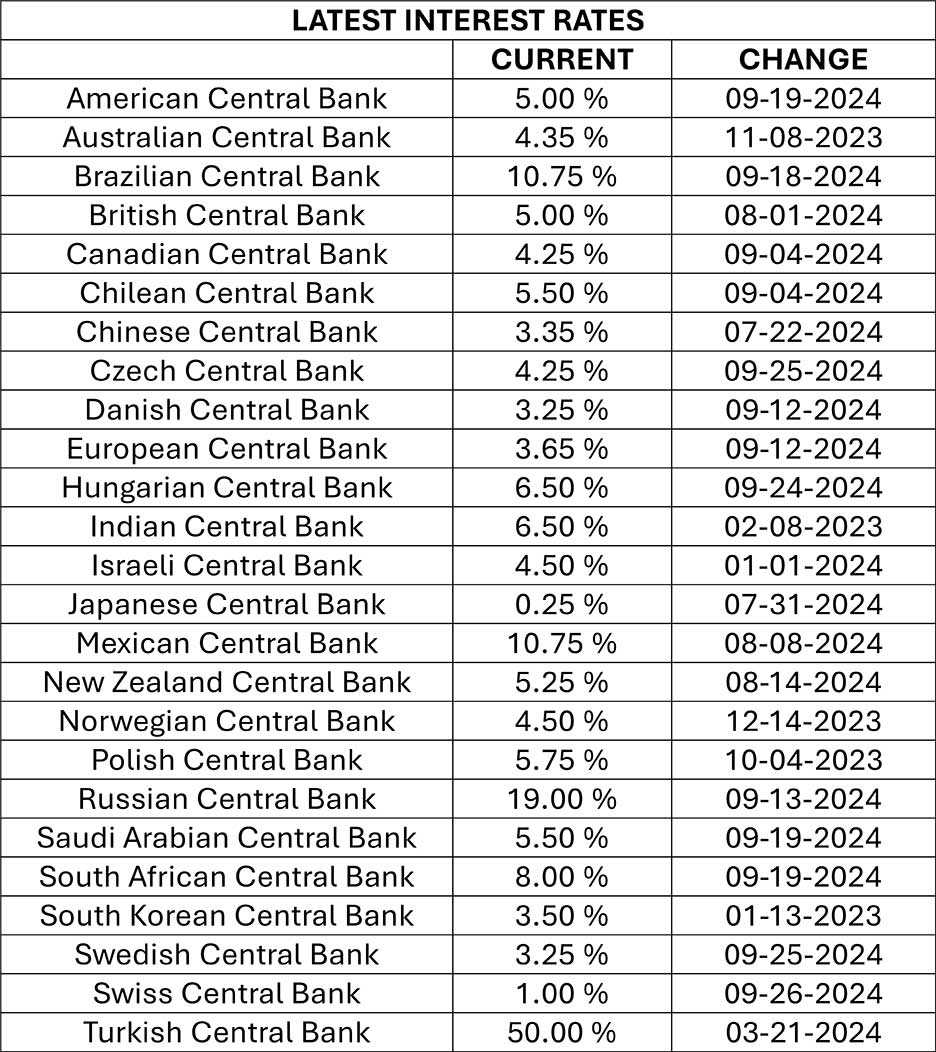

Comparisons to Other Countries

Unlike other nations, such as the US, which recently cut interest rates, Australia’s RBA remains vigilant due to our unique domestic market factors. While the Australian cash rate hasn’t increased as much as other countries, our labour market remains more resilient, with unemployment at 4.2%.

Inflation Outlook and Predictions

The RBA forecasts that the all-important inflation figure might only fall within the target range by late 2025. As inflation remains a top priority, Governor Bullock mentioned that the board is closely monitoring geopolitical risks and uncertainty in global markets.

According to projections by three of the big four banks, rates are expected to stay at 4.35% until February 2025. However, CBA predicts an earlier cut, with the cash rate potentially dropping to 3.1% by Christmas. Further, all major banks are predicting up to five rate cuts next year.

Economic Impact and Government Response

Treasurer Jim Chalmers expressed that the ongoing rate stability is a positive sign, indicating a slowing of inflation. Despite this, concerns remain about how high rates are slowing the economy. Conversely, Shadow Treasurer Angus Taylor argued that Australia lags behind in reducing both inflation and interest rates compared to other developed nations. RBA Governor Michelle Bullock maintains that other countries are dropping rates from a greater height than those reached Australia.

Here’s how we compare to other countries:

The upshot for property entrepreneurs is that, while interest rates remain steady, the RBA’s focus on curbing inflation means that access to finance will likely stay tight. This situation could present opportunities to find motivated sellers under mortgage pressure, so keep an eye out for distressed properties or off-market deals. Be prepared for potential rate fluctuations and stay flexible in your investment strategy to adapt to changing market conditions. Now’s the time to leverage the current climate to negotiate favourable deals and position yourself for future gains.

Units vs. Houses: Is the Price Gap Finally Narrowing?

Over the past decade, units have generally provided a more affordable entry point into property ownership than houses. However, the price gap has widened significantly, with the median house price in April 2024 peaking at a 45% premium over units – a staggering $285,000 difference.

This premium emerged from the pandemic-fuelled housing boom, driven by low interest rates and the demand for more space. However, signs suggest this trend might be reversing, with the house price premium declining to 43% ($280,000) by August 2024.

Why Units Could Be Poised for a Comeback

- Falling Development Approvals: In the last two years, approvals for unit developments dropped by 23%, compared to a 12% fall in house approvals. This decrease is driven by escalating construction costs, higher interest rates, and labour shortages.

- Rising Prices and Supply of Units: The national median unit price increased by 5.2% year-on-year to $658,000 in August 2024. However, with fewer affordable units being developed (only 46% of new units priced below $1 million), demand for established units could rise.

What This Means for Property Investors

Given the reduced supply and rising demand, established units may present a strong investment opportunity as affordability pressures force more buyers into this market. In contrast, new unit developments increasingly cater to higher-end buyers, particularly downsizers seeking premium locations.

Conclusion

The shortage of affordably priced units could fuel demand in the established unit market, leading to potential price growth. Property entrepreneurs should keep a close watch on this trend as it may offer lucrative opportunities for capital growth and yield.

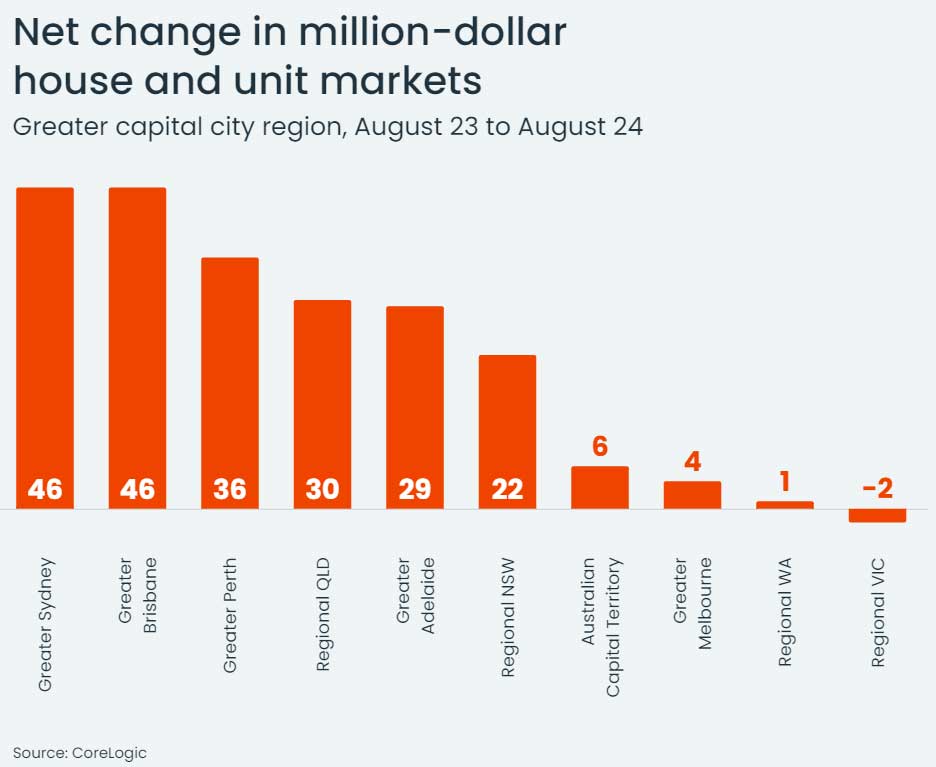

Record Number of Australian Suburbs Hit $1 Million Median Property Value

Recent data reveals that a record number of Australian suburbs have surpassed the $1 million median house or unit value, according to a new report. CoreLogic’s latest findings indicate that 29.3% (or 1,057) of nearly 4,800 surveyed suburbs now have a median property value exceeding $1 million, more than double the 14.3% figure recorded at the start of the pandemic.

Key Findings Across States and Territories

New South Wales (NSW)

Sydney continues to dominate as the country’s most expensive capital city, with 448 house markets and 107 unit markets exceeding the million-dollar median mark. This means nearly half of Australia’s million-dollar suburbs are located in Sydney, with 23 markets re-entering the seven-figure club and 25 joining for the first time, primarily in the city’s South West and Outer South West regions.

Victoria (VIC)

In Melbourne, 191 suburbs met the million-dollar threshold for houses, while 11 did so for units. Overall, dwelling values fell by 1% across Melbourne and regional Victoria since August 2023, with some suburbs dropping out of the million-dollar club. Despite this, several areas, such as Coburg North, Keilor East, and Riddles Creek, have re-entered.

Queensland (QLD)

Brisbane emerged as the market with the largest growth in million-dollar suburbs, tying with Sydney. It now ranks as Australia’s second most expensive capital city, with 46 suburbs (32 new and 14 rejoining) reaching the seven-figure mark. Currently, nearly half of Brisbane’s suburbs have a median house value exceeding $1 million.

South Australia (SA)

In Adelaide, 104 suburbs (36.6% of those surveyed) reached the $1 million mark, an increase from 75 in August 2023. Adelaide’s South region recorded the largest growth in “millionaire” house markets.

Western Australia (WA)

Perth has experienced a 24.2% rise in property values, resulting in 31 house and four unit markets joining the million-dollar club. This surge has made Perth a notable player in the high-end property market.

Tasmania (TAS)

Hobart experienced the biggest decline in dwelling values among capital cities over the past year (-1.2%). Despite this drop, Sandy Bay, Acton Park, and Tranmere remain the only suburbs with a median value above $1 million.

Northern Territory (NT)

Darwin remains the only capital city without any suburbs reaching the million-dollar mark. The highest median value recorded was $939,517 in Fannie Bay.

Canberra (ACT)

Dwelling values in Canberra rose by 1.5% over the past year, pushing six suburbs back into the million-dollar club. Forty-five house markets and just one unit market reached the seven-figure mark.

What This Means for Property Investors

As more suburbs surpass the $1 million mark, affordability pressures continue to intensify. However, with fluctuating growth patterns and some regions experiencing declines, there are still opportunities for savvy investors to capitalise on market shifts. Keep an eye on emerging suburbs that are entering or re-entering the million-dollar club, as they may present potential for strong capital growth in the coming years.

This data emphasises the importance of being adaptable and informed in a dynamic property market where opportunities may arise in both established and up-and-coming regions.

Over 1.6 Million Households Facing Mortgage Stress: What It Means for Property Investors

New research by Roy Morgan has revealed that more than 1.6 million Australian households are “at risk” of mortgage stress, with 29.5% of mortgage holders struggling to meet repayments in the three months leading up to August 2024. This figure, however, represents a slight improvement from July, with a 0.3% decrease following the government’s stage three tax cuts.

Interest Rates: A Key Factor in Mortgage Stress

While the recent data shows a small decrease, the future looks uncertain. The Reserve Bank of Australia (RBA) will play a significant role in determining how this trend evolves in the coming months. If the RBA decides to maintain current rates, the number of households facing mortgage stress may continue to decline. However, should rates rise, more homeowners could be pushed into financial hardship.

The highest level of mortgage stress was recorded in mid-2008 when 35.6% of mortgage holders were at risk. Since May 2022, when the RBA began its cycle of interest rate increases, an additional 852,000 Australians have been added to the “at risk” category, signalling the impact that rising rates can have on household budgets.

Current Situation and Potential Increases

Currently, official interest rates sit at 4.35%, the highest they’ve been since December 2011. Roy Morgan’s data shows that 18.6% of mortgage holders (over a million households) are considered “extremely at risk,” significantly above the 10-year average of 14.5%.

The Role of Household Income and Employment

It’s not just interest rates influencing mortgage stress; household income and employment are critical factors. Despite rising interest rates, Australia’s employment market has remained strong, with 375,000 new jobs created over the past year, providing a buffer against mortgage stress.

Roy Morgan’s Michele Levine emphasised that while interest rates are a significant factor, household income has the most significant impact on whether a borrower falls into the “at risk” category. This means that continued job growth could help moderate mortgage stress levels, even if interest rates rise.

What This Means for Property Investors

For property investors, the increase in mortgage stress among homeowners presents both challenges and opportunities. As more households struggle with repayments, there could be an uptick in distressed sales, potentially providing opportunities to acquire properties below market value. However, rising interest rates could also impact investors’ ability to secure financing, limiting their ability to seize opportunities. This with access to Fuji g sources will be well placed.

That’s a wrap for this week’s Property Edge! As the market continues to evolve, remember that staying informed and adaptable is crucial to success in property investment. Keep an eye out for next week’s newsletter, where we’ll bring you more updates, opportunities, and expert insights to guide you on your property journey. Until then, keep pushing forward and stay ahead of the curve!

Warm regards,

Property Lovers Team