Property Edge

Light At The End Of The Tunnel For Buyers

Welcome to this week’s Property Edge Roundup, your go-to source for the latest insights and updates in the Australian property market. As we navigate the dynamic landscape of real estate, we bring you crucial developments, expert analyses, and trends shaping the future of property investment and homeownership. Whether you’re a seasoned investor or a first-home buyer, our roundup keeps you informed and ahead of the curve. Dive in to explore how new regulations and market behaviours are impacting your property journey.

Light At The End Of The Tunnel For Buyers

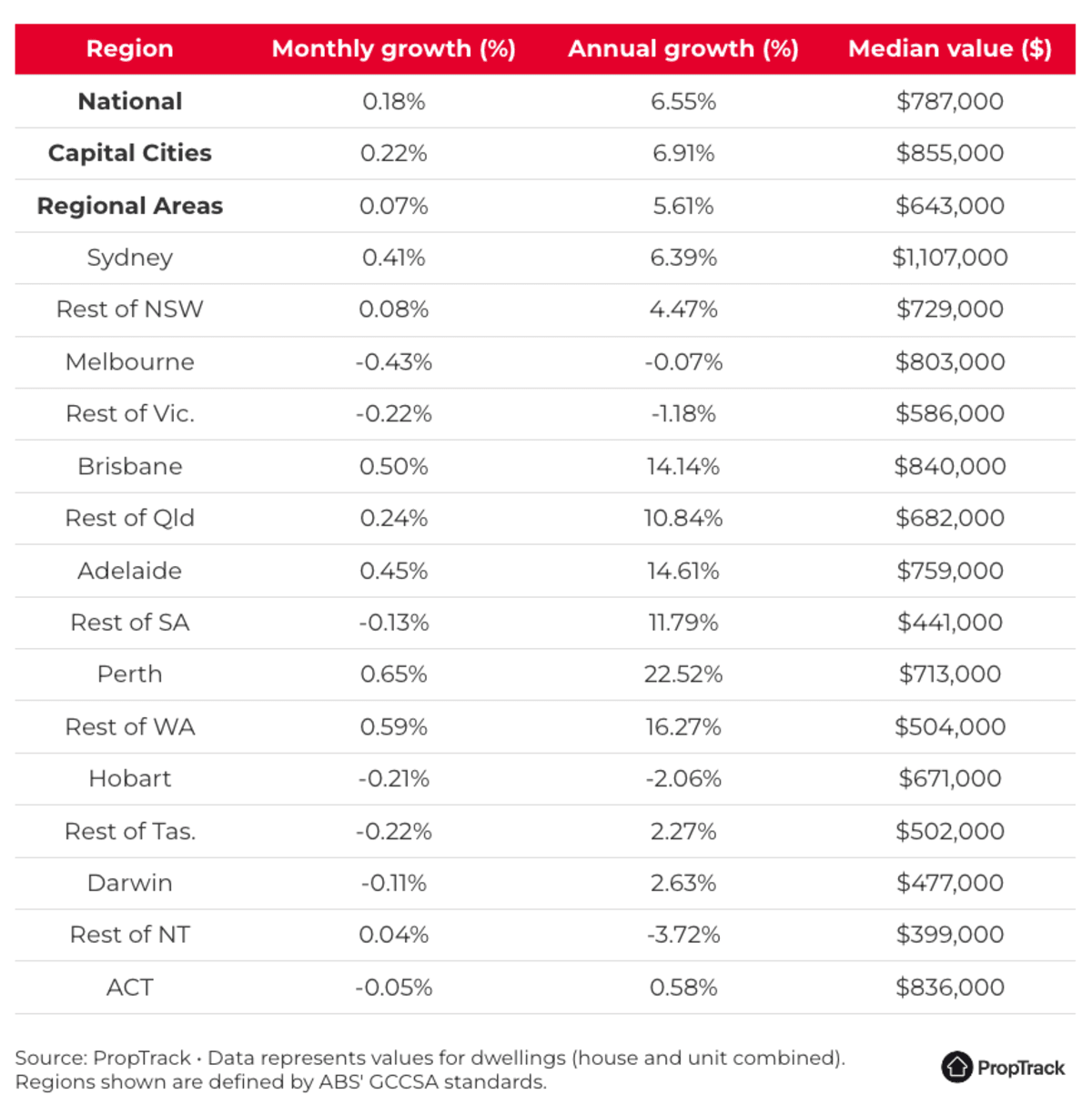

Australia’s median home value reached an all-time high in June, but the rate of price growth has decelerated to its slowest pace in 18 months.

Nationally, home prices edged up by 0.18% in June, according to the latest PropTrack Home Price Index, marking a 6.55% increase over the past year.

While homes have never been more expensive, the slower growth rate offers some relief to buyers wary of being priced out of the market.

Prices have surged in many areas despite borrowing capacities shrinking by about 30% due to 13 interest rate hikes since May 2022. Strong demand for homes has kept prices high, particularly in areas with limited property listings.

However, an increase in available homes in some cities has started to slow down price growth in every capital city, says PropTrack senior economist Eleanor Creagh.

“The pace of growth has eased steadily since the end of the summer selling season as buyers enjoy more options,” she noted.

Moreover, buyers are expected to benefit from the stage three tax cuts effective from today, boosting borrowing capacities by tens of thousands of dollars.

A homebuyer earning 100,000 annually will receive a 2,179 tax cut, increasing their borrowing capacity by approximately 25,000. Similarly, a buyer earning 150,000 will save 3,729, allowing them to borrow about 37,000 more.

While these changes will provide buyers with more spending power, it might also lead to higher prices, according to Ms Creagh.

“From July, tax cuts will lift household incomes, increasing borrowing capacities and buyers’ budgets, further supporting price growth,” she explained.

That said, the increase in borrowing power—expected to benefit first-home buyers the most—won’t cause a rapid acceleration in price growth.

“Although home prices are expected to rise in the coming months, they will likely maintain a slower pace through the seasonally quieter winter period, particularly with increasing uncertainty around the outlook for interest rates,” Ms Creagh added.

Economists at major Australian lenders still anticipate the next move for interest rates to be downward, but a higher-than-expected inflation result has increased the likelihood of an interest rate hike at the Reserve Bank’s next meeting in August.

The RBA kept interest rates unchanged last month, with the board discussing a hike but not considering a cut.

How Home Prices Changed Around Australia in June

Australia’s median home value rose by 6.55% over the past year, with house prices growing slightly faster (6.74%) than units (6.6%).

In some cities, growth has been particularly rapid. Perth’s median house price surged by 23% over the past year to a record high of 762,000. Adelaide’s median house price crossed the 800,000 mark, rising by about 15% to 810,000. Brisbane also saw significant increases, with house prices up nearly 14% and units up almost 17% compared to a year ago.

The Queensland capital is now Australia’s second most expensive city after Sydney, with a combined house and unit value of 840,000 in June, surpassing Canberra (834,000).

In Sydney and Melbourne, an increase in selling activity has improved choices for buyers, Ms Creagh mentioned.

While Sydney home prices rose by 0.41% in June to a new record high, this was the slowest growth rate this year. A typical Sydney house is now valued at 1.428 million, while the median unit price is 818,000.

BresicWhitney chief executive Thomas McGlynn noted a slight market slowdown reflected in lower auction clearance rates and fewer registrations at auctions.

“Inspection numbers remain high, indicating a healthy number of buyers,” he said. “Ever since the interest rate rise cycle began, market sentiment has been largely driven by commentary from the RBA and macroeconomic data.”

Even with a potential interest rate rise, McGlynn believes the market won’t see declining prices but rather stability.

Tax cuts are unlikely to fuel widespread price growth but could support prices for more affordable properties, especially benefiting first-home buyers, he added.

In Melbourne, prices declined for the third consecutive month in June, falling by 0.43% to levels similar to a year ago. This trend is due to a higher number of available homes, Ms Creagh explained.

“Price momentum is weaker in Melbourne as buyers have consistently enjoyed more choice relative to other markets, contributing to softer selling conditions,” she said. The total number of homes for sale in Melbourne has been above the decade average since mid-2023.

In June, prices also dipped slightly in Hobart, Darwin, and Canberra.

Forecast for Slower Price Growth Ahead

Looking ahead, property values are expected to continue rising but at a slower rate compared to the past year.

“Smaller capital city markets like Perth, Adelaide, and Brisbane are likely to maintain their outperformance despite slower growth, as low stock levels intensify competition amid strong buyer demand. Hobart and Melbourne will continue to see weaker price momentum,” Ms Creagh predicted.

PropTrack’s latest Property Market Outlook Report forecasts national price increases of 2% to 5% over the 2024-25 financial year. Perth is expected to see the fastest growth (8%-11%), followed by Adelaide (5%-8%), and Sydney, Melbourne, and Brisbane (3%-6%).

Canberra (2%-5%), Hobart (0%-3%), and Darwin (1%-4%) are expected to experience slower price growth.

Easier Home Building in NSW and WA as New Construction Rules Begin

Brand new regulations in New South Wales and Western Australia aim to simplify home construction as Australia begins its ambitious target of building 1.2 million new homes.

In NSW, landowners can now more easily apply to build dual occupancies and semi-detached dwellings statewide. Similarly, WA’s planning reforms will facilitate building new homes, extending existing ones, or completing smaller projects like patios and carports.

These changes intend to remove local government barriers and streamline planning processes, reducing both time and costs. This aligns with the federal government’s Housing Accord target to build 1.2 million new homes over the next five years to address the housing crisis.

NSW Low-Rise Housing Reforms

The NSW government’s new rules enable more landowners to build granny flats, dual occupancies, and semi-detached dwellings in R2 residential zones across 97% of the state’s local government areas.

Paul Scully, NSW’s Minister for Planning and Public Spaces, highlighted that increased housing choices benefit everyone, from families to renters.

“Dual occupancies provide a viable housing solution for families and downsizers, often being more affordable than detached homes on larger blocks,” Scully said.

However, the rules exclude heritage-listed homes and areas with high bushfire and flood risks.

WA Streamlines Single House Approvals

In WA, new planning rules will expedite local government approval processes for building or renovating homes. The changes limit elected councillors’ involvement in approval decisions for single houses and simple residential projects, except for heritage-listed properties. This empowers planning experts to make final decisions, reducing approval times and costs.

John Carey, WA’s Planning Minister, stated that the reforms will bring consistency across local governments and simplify the process for building or extending homes.

Challenges to Housing Accord Target

While these planning changes are welcomed, concerns persist about achieving the Housing Accord’s goal of 1.2 million new homes in five years.

Cameron Kusher, PropTrack’s Director of Economic Research, expressed doubts about reaching the target by mid-2029, citing the need to reduce construction costs, secure financing for developers, and address planning system inefficiencies.

To meet the goal, 240,000 new homes need to be built annually. However, only about 170,000 homes were constructed last year, marking the lowest level in a decade.

Why Property and Stock Markets Defy Rate Hikes

Australia’s journey out of the inflation battle is becoming a precarious highwire act for the Reserve Bank of Australia (RBA).

Despite numerous interest rate hikes globally, financial and property markets continue to boom, and employment remains robust. This scenario is puzzling central bankers, as traditional economic responses to rate hikes aren’t occurring.

Economic growth has slowed, but employment remains strong. Australia’s unemployment rate is about 4%, similar to the US and UK. Household spending has stayed resilient, benefiting from the best job market in decades.

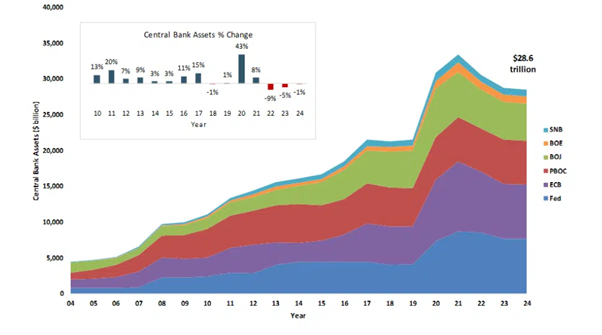

Australian real estate has rebounded, with prices rising every month for the past 18 months. Factors like increased immigration post-pandemic play a role, but a significant influence has been the vast amounts of cash injected into the global economy by central banks over the past 20 years. This has inflated asset prices, including property, stocks, and bonds.

Despite the RBA’s efforts to wind back these cash injections, the global economy remains saturated with excess liquidity, currently around US28 trillion. Australian household wealth has increased significantly, with UBS estimating a rise of 1.3 trillion in the past year, reaching a record 16.4 trillion. However, this wealth increase isn’t evenly distributed, and household debt levels remain high.

RBA Governor Michele Bullock is cautious about further interest rate hikes, prioritising strong employment. Yet, the path out of inflation is risky. Another rate hike could trigger a recession, while holding back could let inflation escalate further.

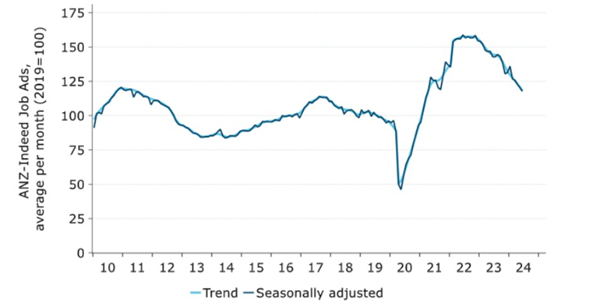

The job market, while still strong, shows signs of weakening. Job advertisements and vacancies have been declining, with vacancies down 17.7% over the year. Household savings, once over 20% during lockdowns, have plummeted to zero, indicating diminishing financial buffers.

The RBA faces the challenge of timing its decisions amidst the lingering effects of pandemic-era cash infusions. The delayed reaction to monetary policies complicates the outlook, as asset prices remain high and inflation persists. The current situation may be unique, but it underscores the complexity of navigating economic recovery.

Thank you for joining us in this edition of the Property Edge Roundup. We hope you found valuable insights to help you make informed decisions in the ever-evolving property market. Stay tuned for our next issue, where we continue to bring you the latest news, expert advice, and trends. As always, your feedback is welcome, and we encourage you to share your thoughts with us. Until next time, happy property hunting and investing!

Warm regards

The Property Lovers Team

PS: NEW WEBINAR ALERT: Want to know how our students are profiting to the tune of multiple 6 figures right now acquiring undervalued distressed properties without finance, any of their own money or even without paying stamp duty or CGT?

At this timely Distressed Property Masterclass, we’ll show you how this is possible.