Property Edge

Dire Housing Shortage Predicted by 2029

Welcome to this month’s edition of the Property Edge Newsletter. As we continually seek out valuable property opportunities for our savvy readers, this issue spotlights affordable capital city suburbs experiencing significant price increases.

Dire Housing Shortage Predicted by 2029

Mike Zorbas, CEO of the Property Council, relayed a concerning forecast from the National Housing Supply and Affordability Council, indicating a significant upcoming shortfall in housing. By 2029, Australia is expected to build only 943,000 of the needed 1,200,000 homes, exacerbating the affordability crisis.

Strategies for Improvement Outlined in New Report

The council’s report, “State of the Housing System 2024,” proposes ten areas for enhancement to address this issue. Key recommendations include increasing social housing investments, improving rental conditions for tenants, boosting construction sector capacity, optimising land use and planning systems, enhancing data availability, and addressing region-specific challenges. The report also emphasises the need for better housing outcomes for First Nations, a re-evaluation of the national housing target, and a taxation system that supports housing supply and affordability.

Focus on Efficient Planning and Innovative Housing Solutions

Zorbas highlighted the importance of planning efficiency, timely land release, and infrastructure development as crucial areas where government action is needed. He also pointed out the potential of alternative housing models like purpose-built student accommodation and build-to-rent (BTR) schemes to alleviate market pressures. Notably, the federal government is reviewing legislation that could greatly influence the BTR sector and possibly lead to the creation of 160,000 new homes by 2033.

Criticisms of Victoria’s Budget Decisions

In Victoria, the budget’s failure to address uncompetitive tax issues has been criticised by Cath Evans, Victorian executive director. The lack of supportive policies is seen as perpetuating a hostile investment environment, driving capital away from the state.

Need for Continuous Dialogue

Zorbas acknowledged the complexity of these challenges and emphasised the importance of ongoing dialogue between the government and the property industry to collaboratively address both short and long-term issues.

Navigating the NDIS Property Market: Opportunities, Risks, and Growth in SDA Investments

As the demand for Specialist Disability Accommodation (SDA) continues to rise, the market landscape for these investments is becoming increasingly complex. With growing interest from a range of investors, including ethical institutional investors and smaller scale operators, the National Disability Insurance Scheme (NDIS) property sector presents both significant opportunities and notable challenges for those not well informed.

Current Market Dynamics

The SDA market has experienced a notable increase in activity, with a surge in the development of high-physical-support units. These developments have reached a three-year high, reflecting a maturing market that began to take shape following the introduction of government-backed NDIS funding for housing. This growth is evidenced by a rising number of SDA apartments in key areas like Melbourne and Sunshine, Victoria, where new facilities are expected to bring substantial rental income.

However, challenges persist, particularly in managing the balance between supply and demand. Recent reports indicate that high physical support units, while crucial, are currently outstripping demand, leading to significant under-utilisation of available SDA spaces. This imbalance is starting to correct itself following recent pricing reforms which have levelled the playing field among different SDA housing categories.

Investment Considerations

Investors looking to enter the SDA market must navigate a series of complexities and costs. SDA properties are highly specialised, tailored to meet the specific needs of their residents, which can vary significantly from one individual to another. This customisation, while essential, adds to the cost and risk of investment, as changes may be needed if the resident changes.

Moreover, the sector is not just about providing housing but also about integrating these facilities into communities, ensuring access to public transport, retail amenities, and employment hubs. The location is therefore a critical factor in the success of SDA investments.

Financial and Regulatory Landscape

The financial landscape for SDA investments is influenced by government funding, which is primarily attached to the NDIS participant rather than the property. This structure can complicate investment returns, as ongoing subsidies and the potential for increased government funding underpin the sector’s viability. Additionally, the separation of property management and support services as mandated by recent legislative changes introduces new operational challenges for providers.

Future Outlook

Looking ahead, the SDA market is poised for substantial growth, driven by limited supply, high demand, and governmental support aimed at reducing red tape and waitlists. This growth promises profitability but comes with its set of demands, particularly in terms of understanding and meeting the specific needs of residents.

Investors must also contend with a steep learning curve, familiarizing themselves with the sector’s compliance and regulatory requirements. This is crucial not only for profitability but also for ensuring that the investments make a meaningful difference in the lives of those they are intended to support.

Conclusion

As the SDA market continues to evolve, it offers a unique blend of challenges and rewards. For property entrepreneurs looking to diversify their portfolios and strategies, SDA presents an opportunity to engage in an investment that can yield both financial returns and social impact. However, success in this sector requires a deep commitment to understanding the nuances of this niche industry.

Title: The Top Booming Yet Still Affordable Areas: Spotlight on Sub-$750K Suburbs

The latest data released by PropTrack has revealed significant price increases in budget-friendly capital city suburbs, where median property values remain under $750,000. Despite rising interest rates and tightening borrowing capacities, these areas have seen some of the highest growth rates, offering potential for first-home buyers and investors.

Key Findings:

Affordable Growth: Many suburbs with substantial price increases are still priced under $600,000, making them attractive to budget-conscious buyers.

Regional Variations: The most significant price surges were noted in Perth, Adelaide, and Brisbane, where some suburbs experienced growth rates higher than 30%.

Capital City Breakdown:

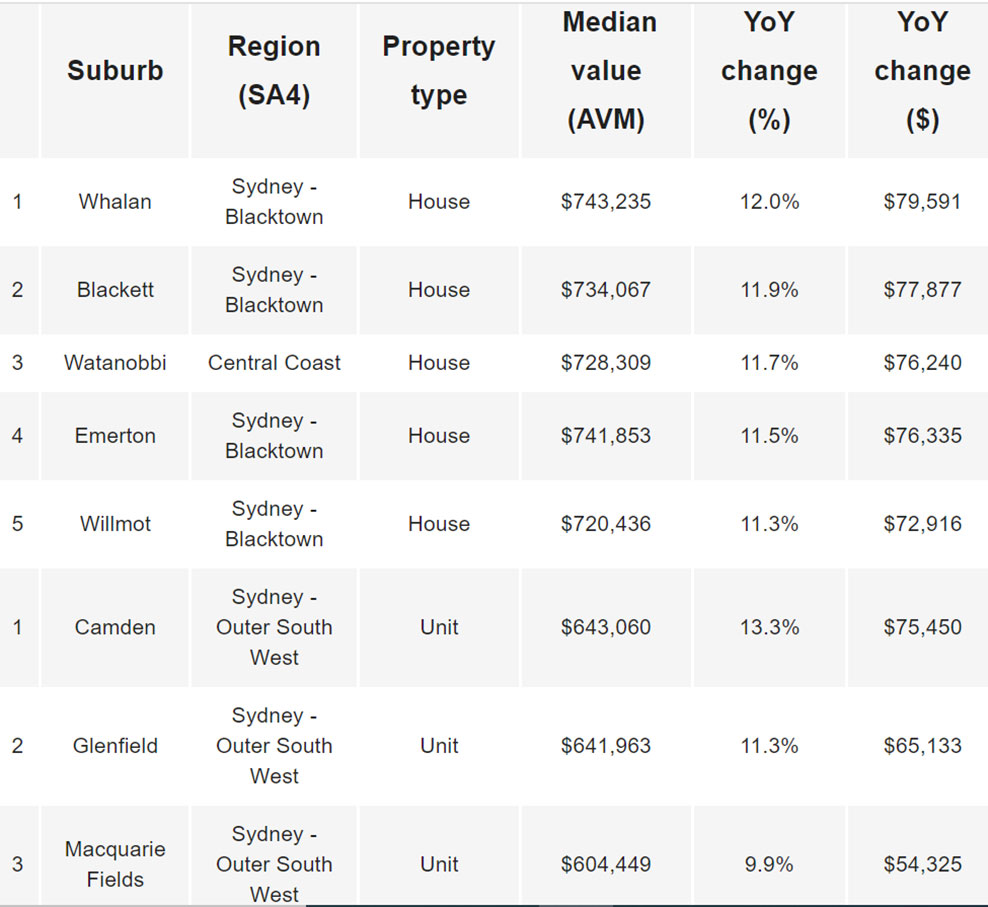

Sydney:

The affordable suburbs with the most considerable price rises are mostly located in the outer regions such as Blacktown and the Central Coast.

Median house values in these areas have increased by approximately $70,000 to $80,000 over the past year.

Melbourne:

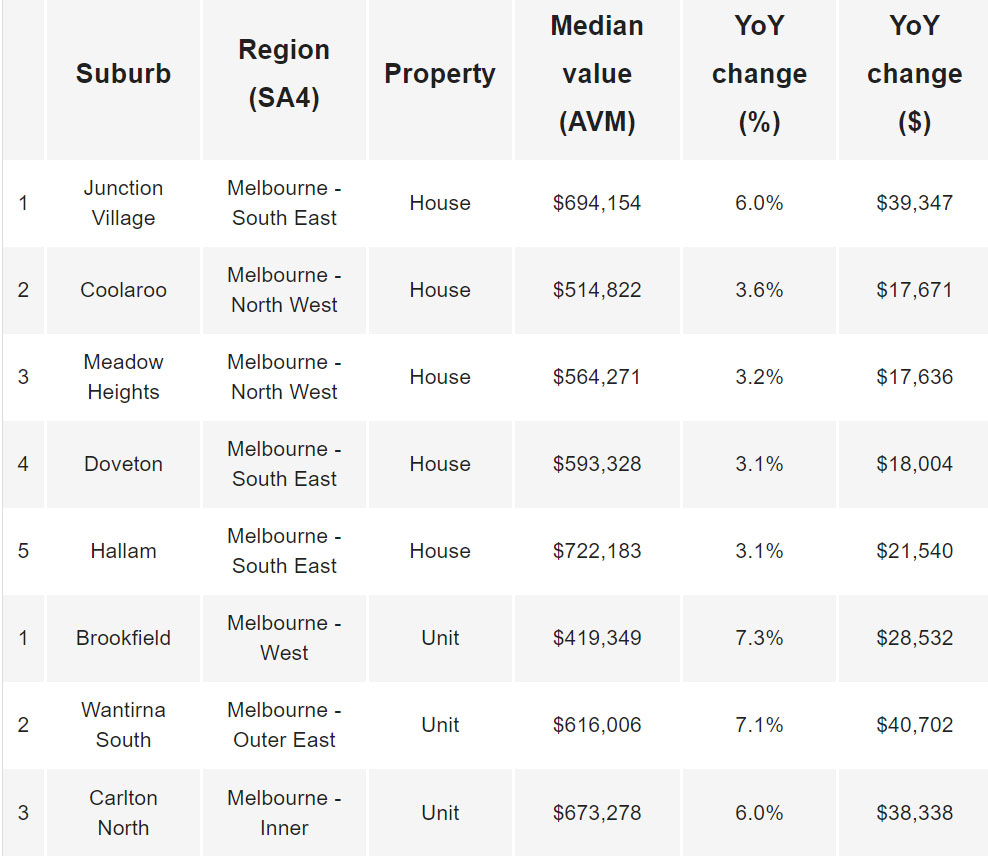

While Melbourne’s market recovery lags, certain suburbs still show promising growth, especially in unit prices in areas like Wantirna South and Brookfield.

Growth in these suburbs is notably higher than the city’s overall rate.

Brisbane:

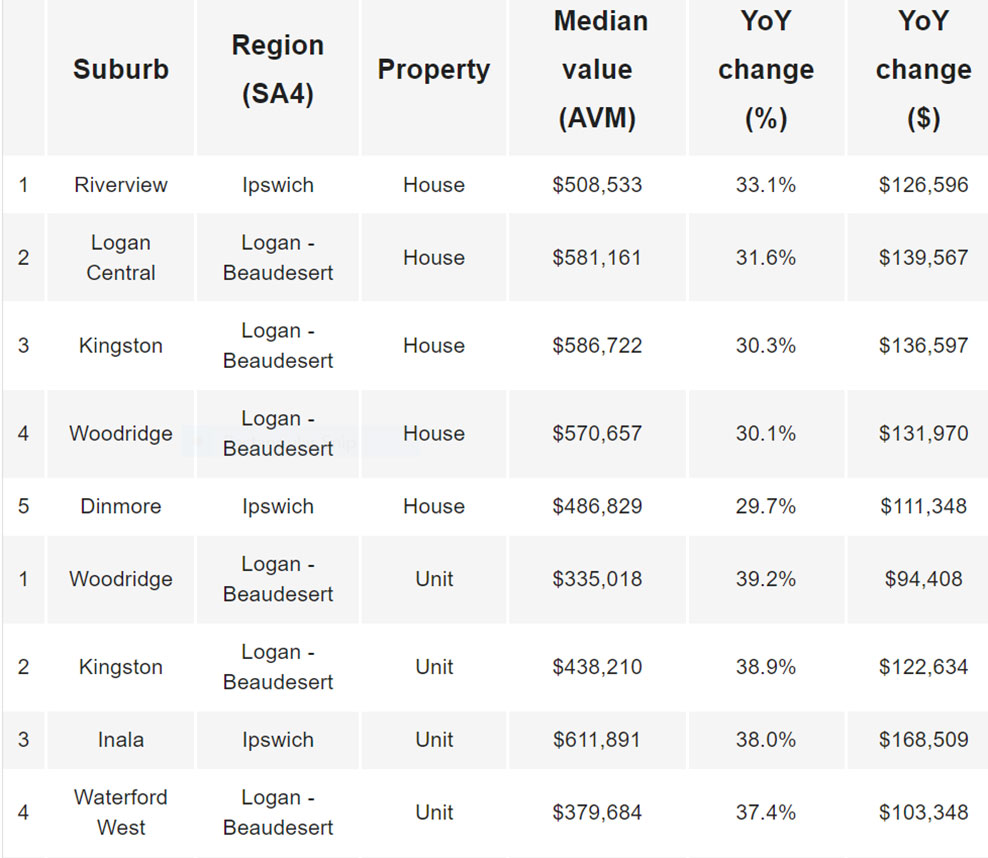

Suburbs around Ipswich and Logan have seen the most dramatic increases, with some areas experiencing up to 39% growth.

This region stands out for its rapid price appreciation, far outpacing the city’s average.

Perth:

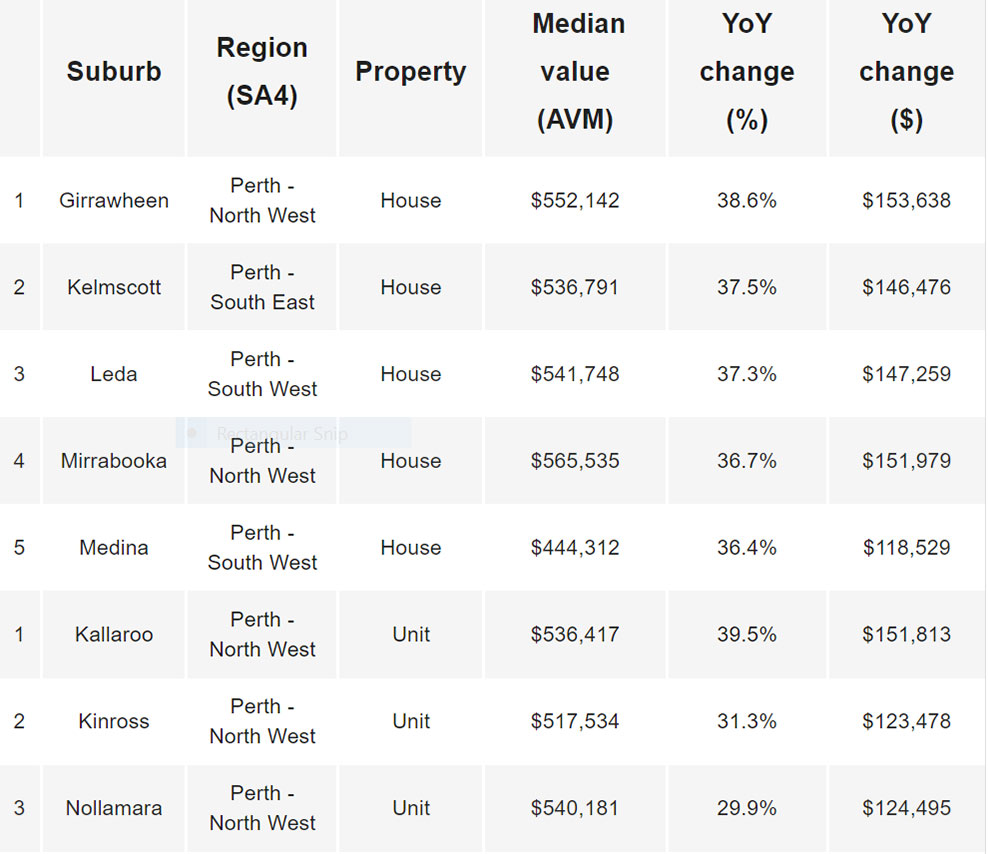

As the strongest performing capital in terms of affordability and growth, suburbs like Girrawheen and Kelmscott have seen increases up to $150,000 in median values.

Perth’s market benefits from strong population growth and limited housing supply.

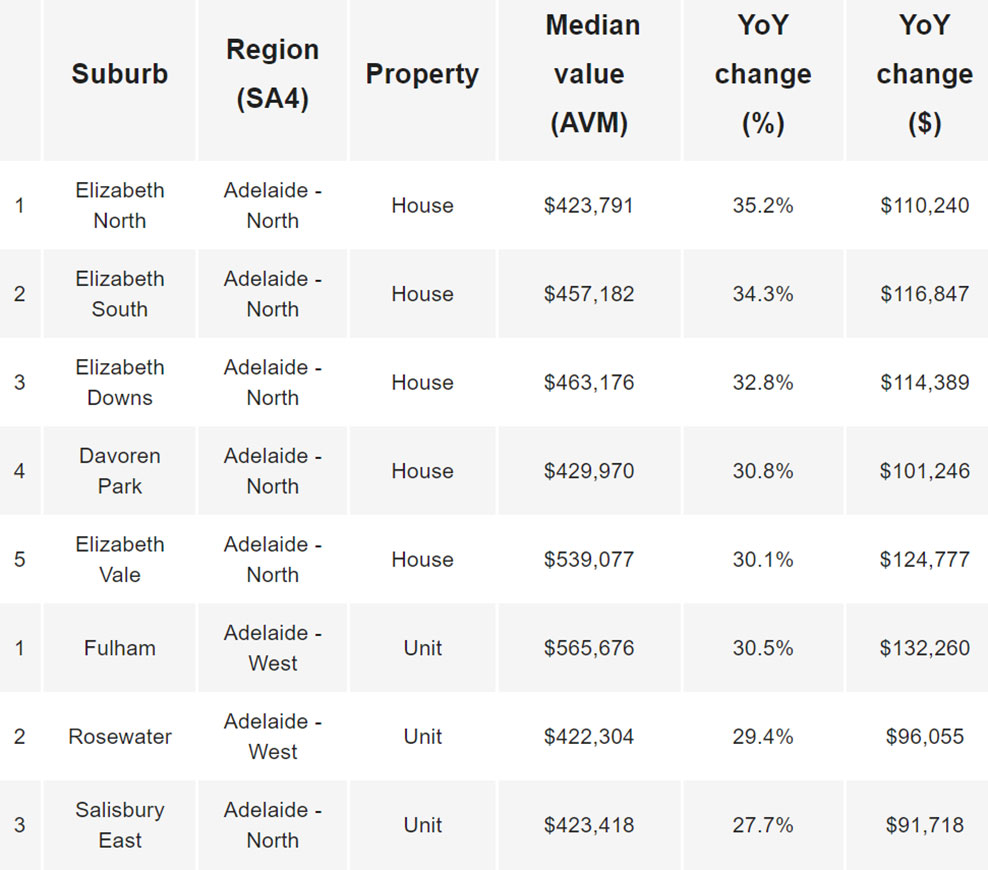

Adelaide:

Northern suburbs like Elizabeth North and Davoren Park lead with growth rates above 30%.

The affordability of these areas combined with high growth rates makes them particularly appealing.

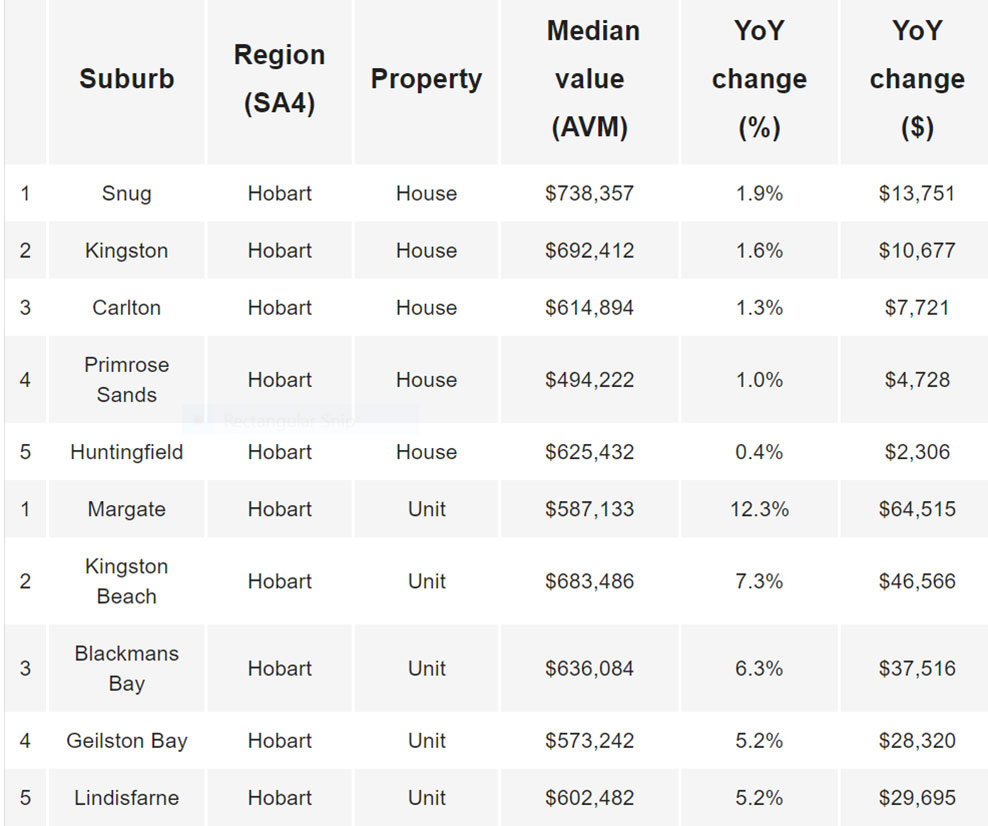

Hobart:

Despite a general downtrend, suburbs like Snug and Margate have seen modest increases in value.

Growth is concentrated on the outskirts and more affordable unit markets.

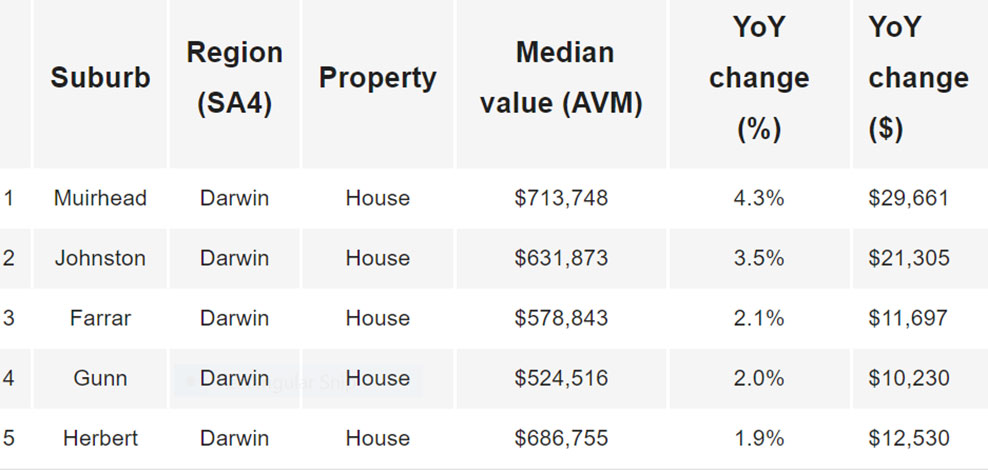

Darwin:

Suburbs within Palmerston, like Muirhead and Johnston, have recorded modest house price increases.

Darwin’s market is expected to rise with government investment and employment growth.

Canberra:

Few suburbs under the $750,000 mark are witnessing growth, with Belconnen and Charnwood showing increases.

The unit market remains a more affordable and growing segment within the capital.

This surge in property values within affordable segments underscores a significant shift in market dynamics, with buyers increasingly seeking value in less expensive areas due to financial constraints and a desire for homeownership. For property entrepreneurs, these areas present an opportunity to capitalise on rapid value growth and strong demand in regions that remain accessible to a broader market segment.

Thank you for exploring this edition of the Property Edge Newsletter. We hope the insights shared here spark your interest in the high-potential, affordable suburbs across Australia’s capitals.