Property Edge

Australia’s Property Market: Trends, Policies & Investment Insights

Welcome to this week’s Property Edge, delivering the latest insights on property trends, economic developments, and policy changes shaping Australia’s real estate market.

Market Trends

Australia’s housing market showed tentative growth after a brief downturn. CoreLogic data recorded a 0.3% rise in national home values in February, ending a three-month stall and bringing prices within 0.1% of their record high from last October. The gains were broad-based, with every capital city (and most regional areas) seeing modest upticks except Darwin and regional Victoria. Notably, previously lagging markets led the rebound – Melbourne and Hobart values each rose 0.4% for the month, breaking Melbourne’s ten-month streak of falls. By contrast, mid-sized capitals that had spearheaded growth earlier (Brisbane, Adelaide, Perth) saw slower monthly increases of around 0.2–0.3% (though Adelaide and Brisbane still top quarterly growth). This shift suggests a rotation, with premium Sydney/Melbourne segments responding quickest to interest rate relief.

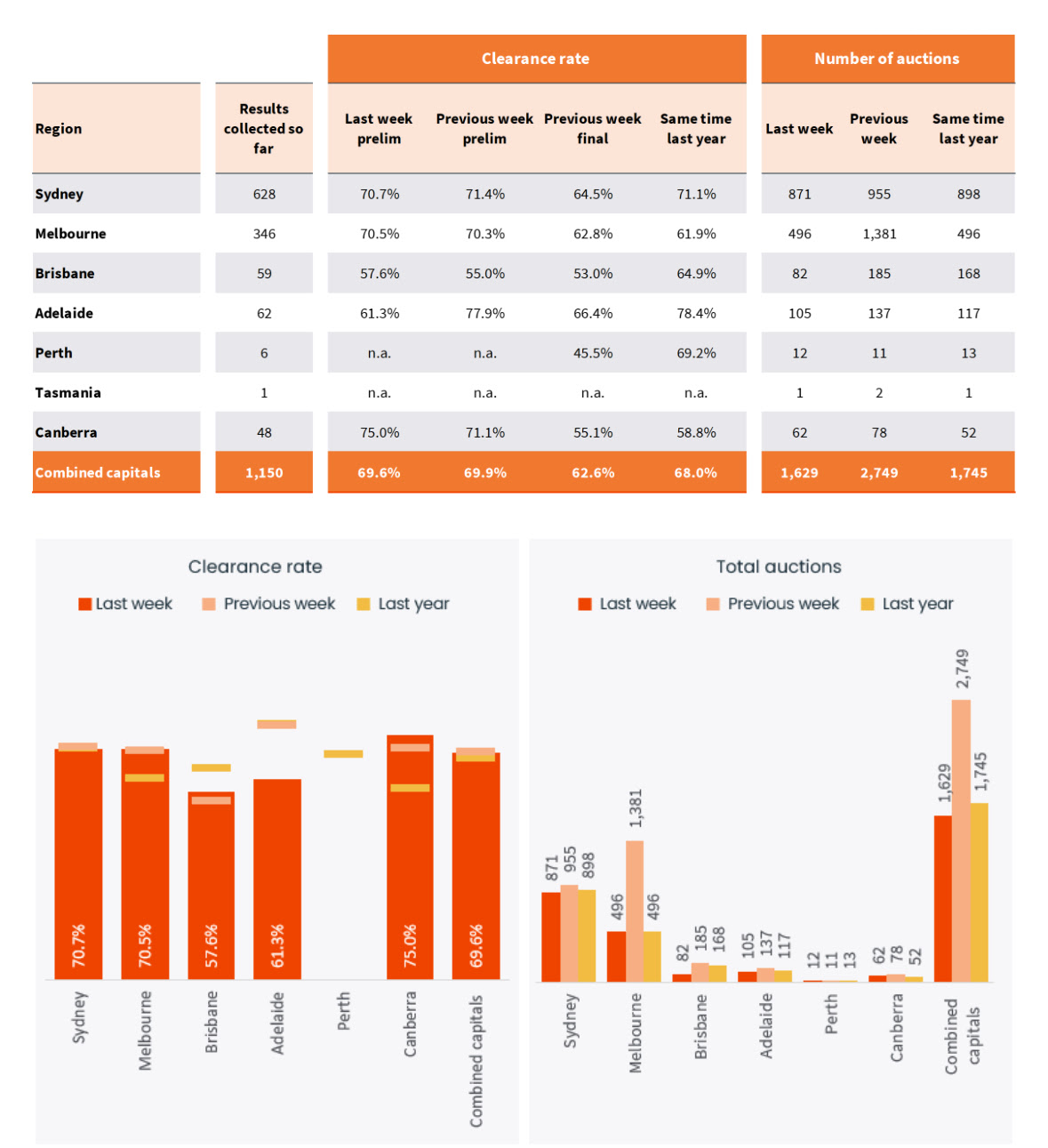

Activity in the property market remains cautious but steady. Auction clearance rates hovered around the high-60s, with the combined capital cities’ preliminary clearance slipping to ~69.6% last week. This marks a slight cooling from earlier in the year, influenced by a long weekend in Victoria and even weather disruptions in Queensland. Despite fewer auctions, buyer turnout is solid in Sydney (around 70% success rate) while some smaller markets like Adelaide have seen clearance rates dip into the low 60s.

The rental market remains very tight but shows early signs of easing. The national vacancy rate edged up to 1.3% in February (from 1.0% in January) as more rentals became available, a slight relief from record lows. Even so, vacancies are still ultra-low in most cities (around 0.6–1.8%), and advertised rents keep rising – nationally up about 1.8% over the past month. Sydney’s rents plateaued (down 0.1%), but other capitals saw monthly rent gains near 1% or more. Industry analysts note that while rent hikes have moderated from the extreme pace of 2021–23, they remain above general inflation. In short, Australia “remains in a rental crisis” amid surging population growth and persistently low housing supply, keeping pressure on tenants despite the slight uptick in vacancies.

Economic Influences

Macro-economic conditions over the past week continue to set the tone for property. The Reserve Bank of Australia’s recent rate cut in February – the first easing in over four years – lowered the cash rate by 0.25 to 4.10%. This policy shift has started to filter through to sentiment and borrowing costs. Mortgage holders are seeing some relief, and buyer confidence is on the mend even though interest rates remain high by recent standards. Notably, consumer sentiment in March jumped to its highest level in three years, with the Westpac-Melbourne index up 4% (to 95.9) following the rate cut and a slowdown in inflation . Easing cost-of-living pressures – annual inflation is now back within the RBA’s target band – and the prospect of cheaper finance have improved households’ outlook . Forward-looking indicators are turning positive: measures of unemployment expectations have fallen to their best levels in two years , reflecting a still-strong jobs market and hopes that a recession can be averted.

Even with these encouraging signs, the broader economic environment remains one of caution. The RBA has signaled it will be patient on further rate cuts, emphasizing that policy is still “restrictive” and that it wants to be sure inflation is decisively trending down before easing more. Markets are currently betting on another rate cut by May if disinflation continues. In the meantime, credit conditions and bank lending appetites are stable, though regulators have highlighted risks around mortgage stress if economic conditions deteriorate. So far, gradual inflation improvement and low unemployment suggest a soft landing scenario, which would be positive for property demand. For property entrepreneurs, the interest rate outlook implies borrowing costs may have peaked, but any relief will likely be incremental – keeping a lid on overly exuberant price growth even as sentiment improves.

Government & Policy Updates

Housing affordability and supply remain in sharp focus for Australian policymakers, with several initiatives unfolding. The federal government’s Housing Australia Future Fund (HAFF) and National Housing Accord notched a milestone this month, approving 29 projects in its first funding round to deliver over 2,100 new social and affordable homes. While welcome, this is just a drop in the bucket relative to Australia’s housing shortfall – the nation is building far fewer homes than needed. A target to add 1.2 million homes from 2024 to 2029 under the National Housing Accord is falling behind, as construction industry challenges (rising costs, labour shortages) continue to stymie supply. State governments are also stepping in with measures to boost development. For example, Western Australia announced planning reforms to cut red tape for community housing projects; from May, apartment developments that include at least 5% affordable housing will qualify for a fast-tracked approval pathway. Such moves aim to accelerate housing construction, particularly for vulnerable groups, amid an acute shortage of rentals and affordable dwellings.

Housing policy is also heating up as a federal election issue, spurring new proposals and debate. One high-profile idea from the opposition is to allow first-home buyers early access to their superannuation savings to help finance a house deposit. This “super for housing” plan has drawn both support and criticism – proponents argue it would help young buyers overcome the deposit hurdle, but economists warn it could simply boost purchasing power and push prices even higher. Critics, including government ministers, note that raiding retirement funds may undermine long-term savings and do little for those who lack substantial super to begin with. On the regulatory front, the federal government is moving ahead with a two-year ban on foreign buyers purchasing existing residential properties, effective 1 April 2025. Foreign investors will still be welcome to invest in new developments, but blocking them from established homes is intended to ease competition and free up roughly 1,800 homes per year for local buyers. Additionally, authorities are tightening rules to prevent “land banking” – foreign owners holding undeveloped land idle – by imposing development timelines and vacancy fees. These policy measures underscore a broad push by governments to improve housing accessibility and tame excess demand, which could gradually create a more balanced market for developers, investors, and homebuyers.

Stay tuned for next week’s Property Edge, keeping you ahead of market trends and developments to empower your property decisions.

Important:

Find renovation property deals to flip for profit using potentially none of your own money with commercial funding (new funding available), Our research tool helps you find profitable deals to flip with 20% profit so you qualify for commercial finance (newly available for renovation deals).

Access FastProperty.AI for free. No credit card required..