Property Edge

2025 Housing Market Outlook: Winners and Losers Across Australia

Welcome to Property Edge! This issue dives into easing inflation, mortgage stress relief, and what’s next for interest rates. Here’s what you need to know.

2025 Housing Market Outlook: Winners and Losers Across Australia

Property prices across Australia are set to follow a mixed trajectory in 2025, with significant gains in smaller capitals offset by further declines in Sydney and Melbourne, according to SQM Research’s Housing Boom and Bust Report 2025.

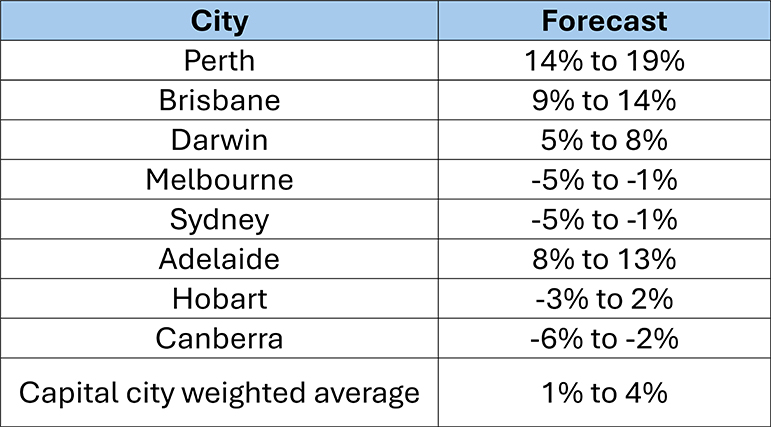

The report projects a national average increase of 1-4% in capital city property prices. However, Sydney and Melbourne are forecast to face declines of up to 5%, even if the Reserve Bank of Australia (RBA) implements a cash rate cut of 0.25 to 0.5 percentage points mid-year.

Housing Boom & Bust Report 2025

Source: SQM Research

Diverging Market Trends

Louis Christopher, founder of SQM Research, attributes the national growth to strong performance in smaller capitals like Perth, Brisbane, and Adelaide, which are expected to experience robust price increases. “Sydney and Melbourne prices are already falling, and this trend is likely to continue until rate cuts take effect,” he explained.

While a rate cut could stabilise Sydney and Melbourne markets in the latter half of the year, Christopher predicts these gains won’t be enough to offset early-year declines. He cites factors such as rising distressed sales, high inventory levels, and affordability constraints as key drivers of the downturn in these cities.

Boomtowns Lead the Charge

Perth is forecast to lead the nation, with property prices projected to rise by an impressive 14-19% in 2025. Brisbane and Adelaide are also set for significant growth, with expected increases of 9-14% and 8-13%, respectively.

Christopher highlights strong population growth and limited housing supply as the main catalysts for price surges in these cities. “Perth, in particular, shows no signs of trouble. When mining towns start to struggle, it usually signals a market shift—but we’re not seeing that here,” he noted.

Mixed Views on Sydney and Melbourne

Opinions are divided on the extent of declines in Sydney and Melbourne. AMP’s deputy chief economist Diana Mousina anticipates only modest falls in Melbourne, with Sydney potentially holding steady due to ongoing housing undersupply.

“Sydney remains the most unaffordable market in Australia, which could temper growth,” Mousina said. “However, I find it unlikely that prices will record a net fall over the year.”

CBA’s chief economist Gareth Aird also expects Sydney to slightly outperform Melbourne, though affordability pressures will continue to weigh heavily on both markets.

The Role of Interest Rates

The RBA’s monetary policy decisions will play a critical role in shaping the market. Christopher suggests that if no rate cuts occur in 2025, national dwelling prices could stagnate or decline, with Sydney and Melbourne facing sharper falls of up to 8% and 7%, respectively.

Regardless of interest rate movements, smaller capitals are expected to dominate growth.

Inflation Drops to 3-Year Low: What It Means for Interest Rates and Homeowners

New data from the Australian Bureau of Statistics (ABS) shows inflation has slowed to a three-year low, rising just 2.1% in the year to October. This marks a return to the Reserve Bank of Australia’s (RBA) target range of 2-3%, the lowest inflation rate since July 2021. However, economists believe the RBA may still delay cutting interest rates until mid-2025, despite mounting pressure.

Key Inflation Drivers and Trends

The slowdown in inflation is largely due to significant drops in electricity prices (-35.6%) and automotive fuel, which had a major impact on the Consumer Price Index (CPI). On the other hand, prices for food, recreation, and alcohol continued to rise, keeping underlying inflation pressures high.

Homeowner Stress Intensifies

Rising interest rates have left many Australians in financial distress. A Finder survey revealed that one in seven homeowners may have to sell their homes or apply for hardship relief by February if rates don’t fall. Additionally, two in five borrowers are cutting back spending to manage mortgage payments, with many having depleted their savings.

The RBA’s Dilemma

Despite inflation being back within target, economists suggest the RBA may remain cautious. Underlying inflation pressures, combined with government energy and rent relief programs temporarily easing costs, make an immediate rate cut unlikely. The risk, however, is that prolonged high rates could push the economy into recession.

Rate Cut Predictions

Economists are divided on when the RBA will cut rates. Some of Australia’s major banks predict a reduction as early as February, while others suggest May. Bendigo Bank forecasts a 35 basis point cut in May to initiate a cycle of rate reductions.

Outlook

While falling inflation provides some relief, high interest rates continue to strain households. The RBA’s next steps will be crucial, balancing economic growth with the risk of further financial hardship for Australians.

Inflation Falls, but RBA Sticks to High Rates

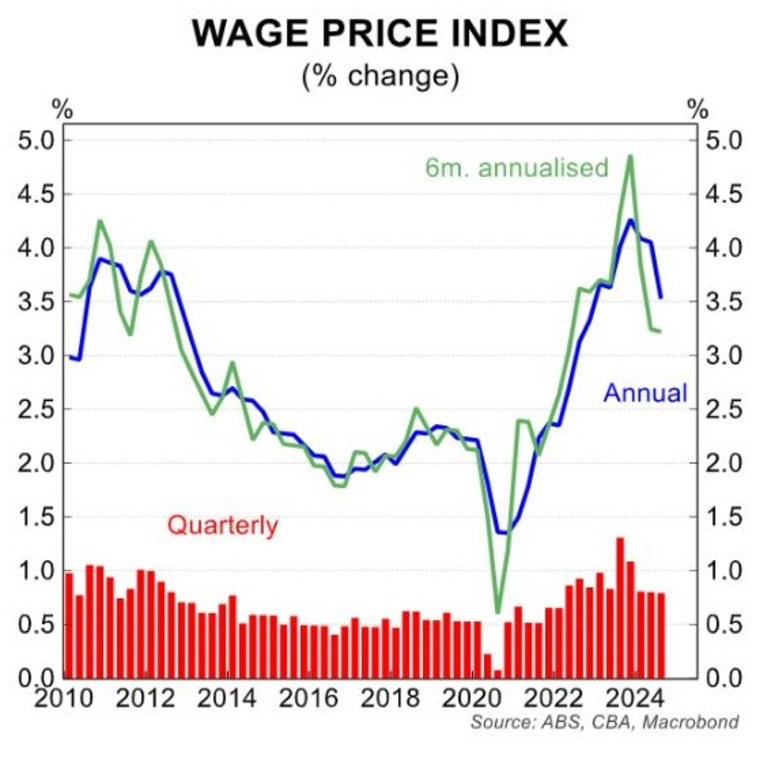

Inflation in Australia is dropping fast, falling well within the Reserve Bank of Australia’s (RBA) target range of 2-3%. Recent data shows wage growth has stalled at 3.2% for the past nine months, a key driver of the inflation slowdown. Despite this, the RBA has kept interest rates high, citing concerns about productivity and economic capacity—concepts that many argue don’t align with Australia’s unique economy.

Unlike other countries, Australia’s growth is driven by immigration and labour market expansion, which keeps wage pressures low. This means falling wages lead directly to falling inflation. Yet the RBA is holding onto outdated theories, which critics say risks dragging the economy deeper into a technical recession that’s already lasted nearly two years.

For property owners and buyers, the RBA’s stance means continued pressure. High interest rates are squeezing mortgage holders and slowing the market. While rate cuts seem inevitable at some point, the timing remains uncertain, leaving many Australians feeling the strain. The big question now is whether the RBA will adjust its approach to match the reality of falling inflation—or stay the course.

Mortgage Stress Eases, but Rate Cuts Remain Crucial

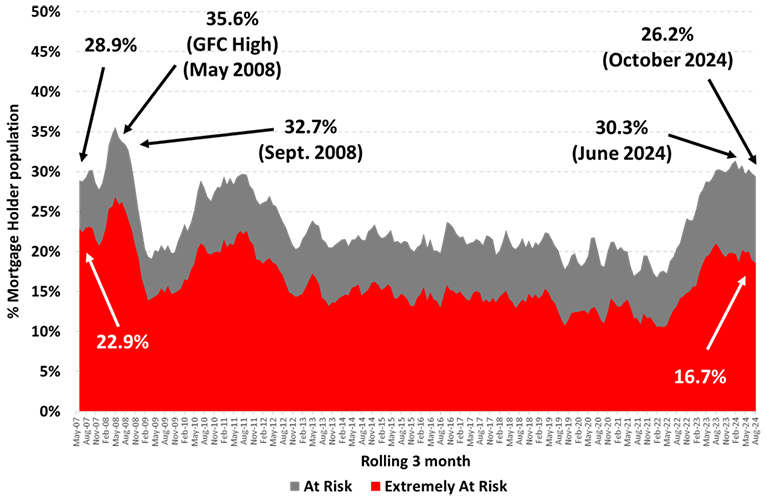

The latest Roy Morgan research brings some positive news for Australian homeowners: the proportion of mortgage holders “at risk” of mortgage stress has fallen to 26.2% in the three months to October. This is the lowest level since February 2023 and a 4.1% drop since June, largely thanks to Stage 3 tax cuts that have boosted household incomes.

Despite the improvement, challenges remain. Around 1.49 million Australians are still “at risk,” with 16.7% classified as “extremely at risk.” Since the Reserve Bank of Australia (RBA) began raising rates in May 2022, over 680,000 additional mortgage holders have been pushed into the “at risk” category.

Michele Levine, CEO of Roy Morgan, emphasised that while rising incomes and falling inflation have eased some financial pressures, household income tied to stable employment remains a critical factor in determining mortgage stress levels.

Projected Relief on the Horizon

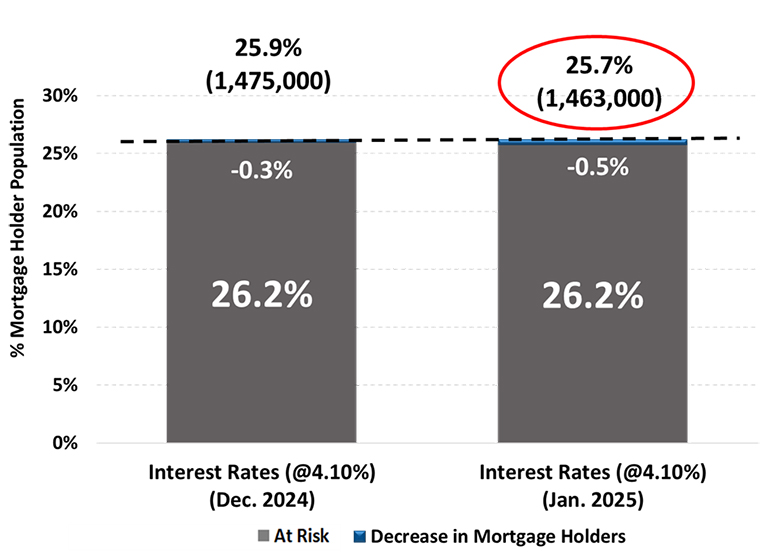

With inflation now within the RBA’s target range of 2-3%, optimism is growing for rate relief. Roy Morgan’s models predict that a potential 0.25% interest rate cut in December could reduce the proportion of “at risk” borrowers to 25.9% by year-end. Additional cuts in early 2025 could lower this figure further to 25.7%.

While a rate cut would provide immediate relief, Levine highlighted the importance of employment stability and wage growth in ensuring long-term financial health for homeowners.

That’s it for this edition of Property Edge! Stay tuned for more key updates shaping the property market.

Warm Regards,

Property Lovers